Topic 2: INDIA’S ENTRY TO JP MORGAN INDEX

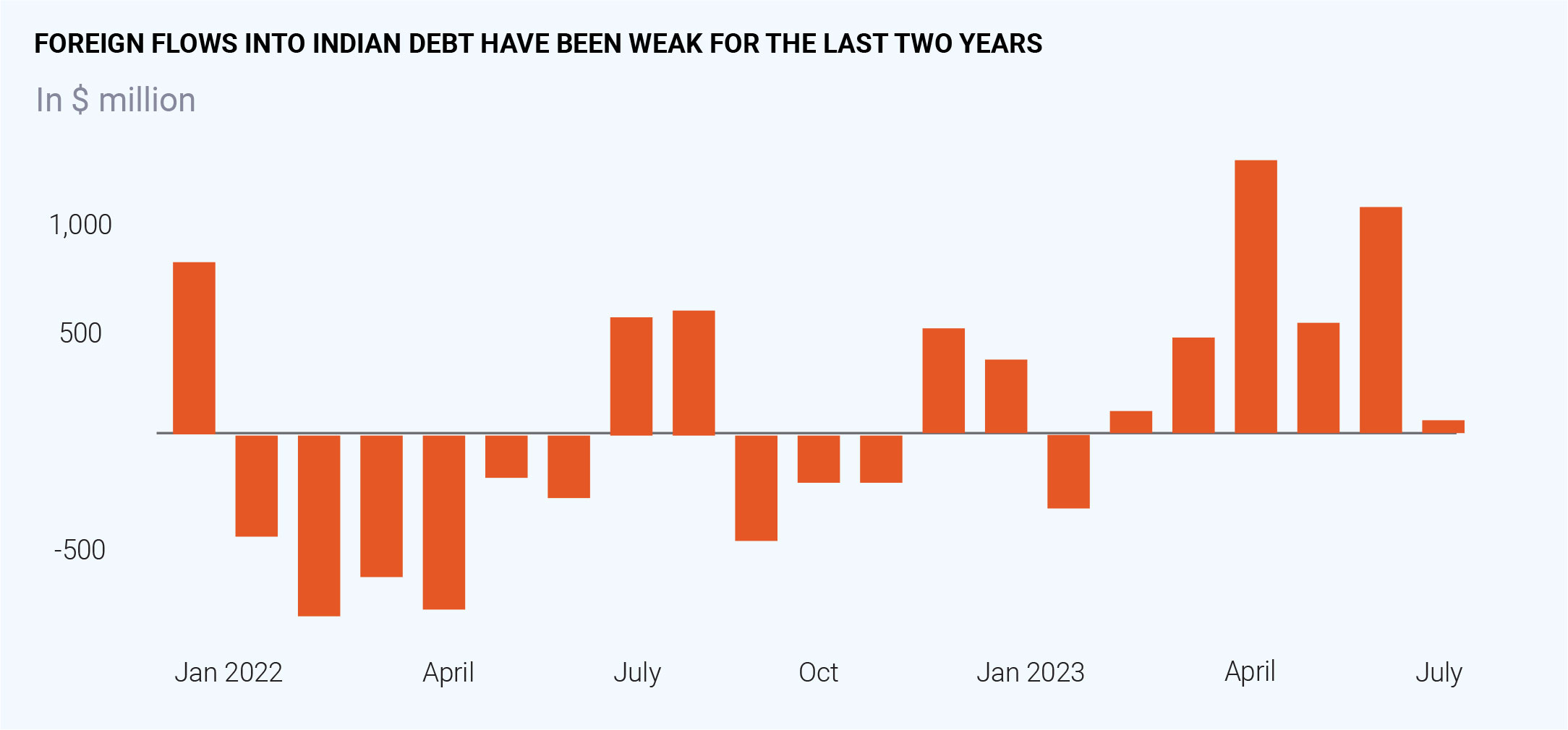

The good news for the Indian debt market as JP Morgan Chase & Co announced, to include Indian government bonds in its emerging markets bond index from June 2024. This move would attract more foreign inflows into the domestic government securities market. Starting from 28 June 2024, India will be included in the GBI-EM Global Index Suite is expected to reach a maximum weight of 10% in the GBI-EM Global Diversified Index (GBI-EM GD). A total of 23 Indian government bonds with a notional value of $330 billion are index-eligible. Bonds will be added in a staggered manner over the period of 10 months through 31 March 2025, (including 1% weight per month). The value of the JP Morgan Index is $240 billion and India will be 10% of it, that is $24 billion. This will reset the base rate for India which brings down the yields and also cuts down the borrowing. Greater foreign inflows next year will result in increased demand for Indian government bonds. In 2024-25 Centre would borrow a smaller amount compared to Rs 15.43 lakh crore this year as the fiscal deficit target could be around 5.5% of GDP. This dual movement of increased demand for and possibly reduced supply of government bonds. Then the demand for Government securities exceeds supply, in turn bond yields will fall. The capital inflows mean a stronger rupee, in this case, the US dollar’s strength and rising crude oil prices will be headwinds for the short term. The central bank has to play an important role in absorbing any heavy inflows. The key challenge for the Indian debt market would be the high beta due to international factors and also Indian economic volatility would not be acceptable. After this inclusion, India could see other index providers like FTSE Russel and Bloomberg Global Aggregate Index. FTSE Emerging Markets Government Bond Index Capped oversaw total funds of $1477 billion which is 6 times of JP Morgan GBI-EM GM. India could anticipate its inclusion in many other indices in the coming years.