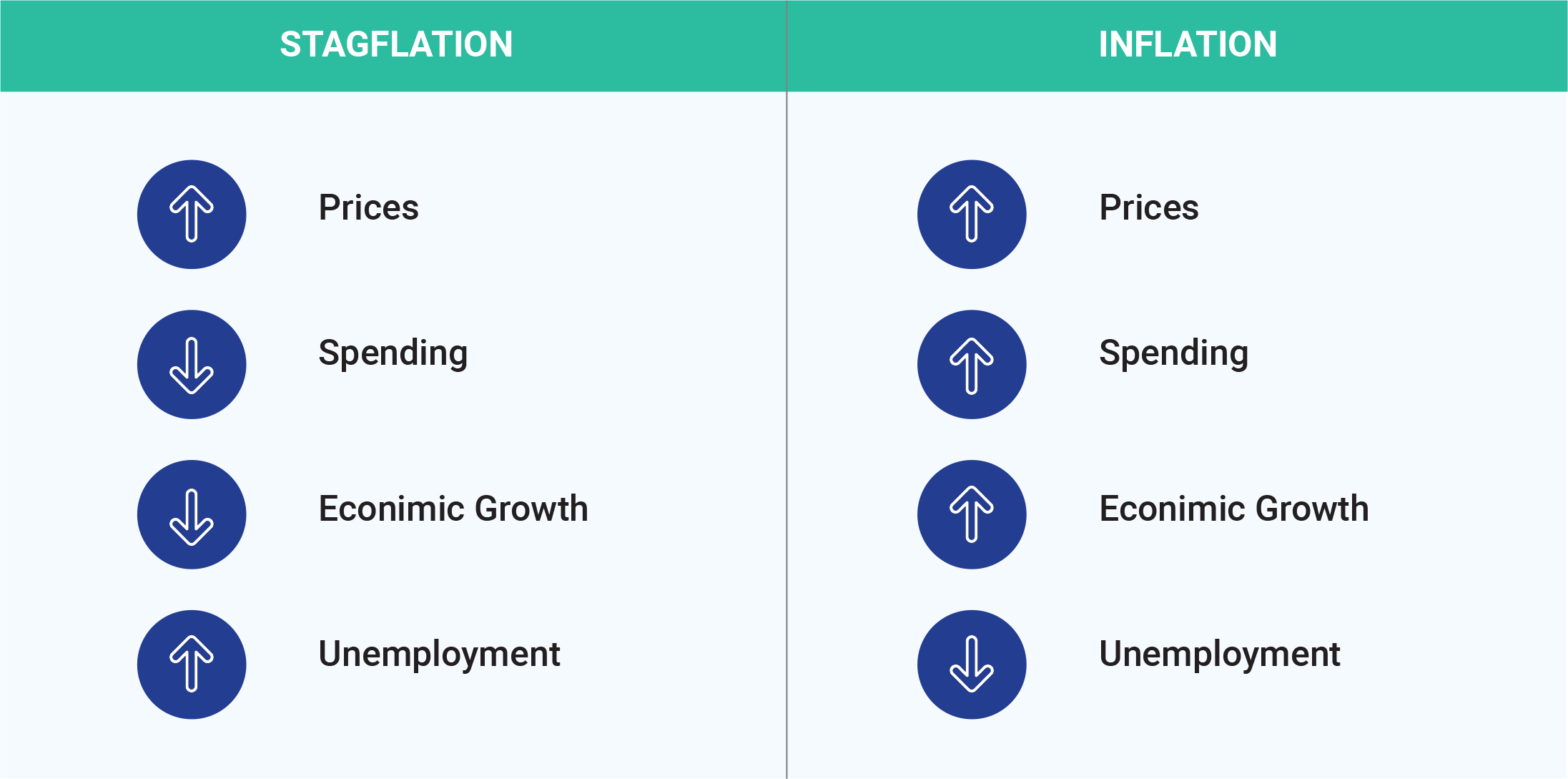

Topic 3: INFLATION VS STAGFLATION

The recent RBI bulletin used the term ‘Stagflation', RBI stated that India is in better shape and would not go into stagflation. Stagflation risk remains low for India with a probability of only 3% with an easing of financial conditions, stability of the INR/USD exchange rate, and steady domestic fuel prices, a study conducted by RBI stated. India's retail inflation in July jumped to 7.44% from 4.87% in June, mainly due to the soaring price of tomatoes, vegetables, and other food items. While core inflation witnessed a moderation (in July), headline inflation is expected to average well above 6%. As the world is fighting inflation taking all the measures like reducing the interest rates, if despite threshold of rate cut is met by the country then they would be in stagflation. The risk of stagflation across the world economies varies significantly. China is currently in a deflation state as consumer prices have fallen for the first time in over two years. Latin American countries are promptly hiking rates to double digits and succeeded in controlling their inflation for the time being. UK and Germany are facing stagflation despite of rate cut the inflation numbers are above the target. Despite continuing to expect the UK to steer clear of a recession in 2023, GDP is projected to grow barely by 0.4% this year and by 0.3% in 2024, with the outlook remaining highly uncertain. Germany with a sharp decline in Industrial production would again fall into recession. Inflation in the US is falling which inhibits stagflation for now. Volatility in food prices and energy prices are major threats to the core inflation now. European economies are more vulnerable due to the ongoing Ukraine war in the region which affects the commodity prices. The Russian grain deals and disruptive weather conditions across the world would push the inflation higher which would increase the risk of stagflation across the globe.